Shurley on Cotton: Prices Still Low, but Find Stability

January 25, 2016

January 25, 2016 By Dr. Don Shurley

Old crop March 2016 futures closed last week at 62.45 cents – up 1.04 cents for the week. After recently threatening the 61-cent area and even challenging 60 cents in late September, prices now seem to have found a little support and – dare we say – upward momentum.

The decline of the past two weeks has largely been due to global and China economic concerns and declining oil prices – all of which are impacting the stock market and other commodities.

The 61-cent area seems to be holding. While this is still far below what makes everyone happy, considering this market was once thought headed for the 50s, we take any good news we can find.

Longer term, prices still likely face resistance around 64 to 65 cents. If you have cotton in Loan or otherwise in storage, keep mindful that rallies to the mid-60s or higher likely represent good price risk management opportunities. In the Loan, also be mindful of MLG or equity opportunities. And remember, it’s the “total money” you are trying to achieve.

In addition to price movement, basis has been improving and fiber quality premiums have been strong. Basis in the Southeast is currently +175 March for base grade 41-4/34 and premium +325 for 31-3/35. This Southeast basis has improved +50 points in recent weeks. Premium for 31-3/25 is +275 points in the Mid-South and +150-200 points in Texas. This is USDA-AMS data.

Estimates of possible 2016 cotton acreage will begin to get attention over the next few weeks. The National Cotton Council estimate will be released during its February annual meeting, and USDA’s first estimate will be released on March 31.

Growers planted 8.58 million acres in 2015. Early guestimates for 2016 have been mostly 9.0 to 9.5 million acres, with some estimates below 9.0 and some closer to 10 million.

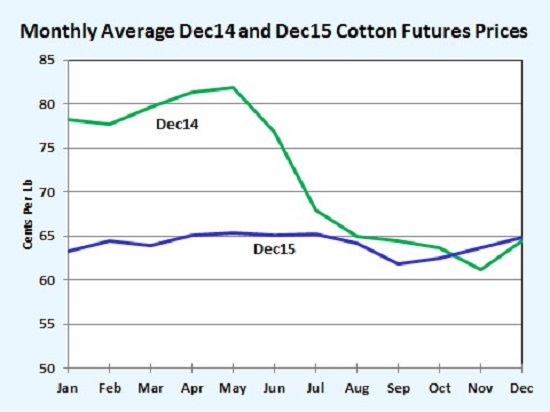

December 2016 futures prices are currently close to 63 cents – a little lower than where December 2015 futures were last year at this time. Prices for 2016 could take a path similar to the 2015 crop. The 2015 crop never could break out of a range of mostly 62 to 66 cents. The factors in play for the 2016 crop year will have to break this rut.

The cotton marketing loan LDP provides protection from low prices. But low prices do not necessarily translate into low/lower acreage. The LDP/MLG acts to insulate the grower from low World and U.S. prices. When the World price (A-Index or Far East Price) falls below 72 cents, U.S. cotton futures will be about 67 cents, and the LDP increases as price declines.

Although cotton prices have remained disappointing and low, it is relative prices that are important. Compared to last planting season, cotton compared to corn is about the same. But when cotton is compared to soybeans, cotton has gained.

Despite disappointing prices, in addition to LDP’s, cotton has also benefited from a strong basis and good premiums for better fiber quality. There are no guarantees this will continue, but it is something to be considered. Newer/recently released varieties also offer both high yield potential and excellent fiber quality.

Shurley is Professor Emeritus of Cotton Economics, Department of Agricultural and Applied Economics, University of Georgia