Once Again, India’s Outlook Hinges on Export Policy

India today enjoys a unique position in global cotton. It is the second-largest grower and exporter of cotton and is surpassed only by China as a consumer of cotton. It is also one of the significant exporters of cotton yarn and garments.

More than 5.8 million farmers cultivate cotton in India and as many as 50 million people are employed, directly or indirectly, by the cotton industry. Government initiatives like the Technology Mission on Cotton and Technology Upgradation Fund Scheme have improved the marketability of the cotton produced, and helped in modernizing and upgrading of the ginning and pressing factories. These initiatives have led to appreciable improvement in the quality of cotton bales, which in turn have proven beneficial for the textile industry. Furthermore, growing disposable incomes have also accelerated domestic consumption, increasing demand within the country as well.

It is a challenge to provide accurate statistical data for cotton acreage and production in India. There are differences in the production data presented by states, and the production data assessed by the Cotton Advisory Board with regard to consumption and stock on hand, thus making it difficult for the domestic and international cotton industry to formulate business plans.

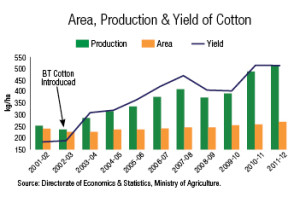

In 2011/12, a record 12 million hectares were planted by farmers, lured by lucrative returns.

However, the hip-hop in Government export policy and high volatility in price has prompted Indian farmers to look at other alternatives such as maize, groundnut, guarseed and soybean in some areas.

As of September 14, cotton has been planted on 11.4 million hectares, slightly lower than a year ago, but above the last three year average of 11 million hectares.

But acreage is not the only matter of concern; it is output and quality of the crop. Prospects for a good yield depends on rainfall in late September and early October when the crop enters the boll formation phase.

According to the latest updates of the Cotton Advisory Board, cotton output for 2011-12 season is revised upward to 35.7 million bales from its last estimate of 35.3 million bales (of 170 kg each). The ending stocks figures for the 2011-12 season that would end in September, has been revised upward to 2.8 million bales from previous estimates of 2.5 million bales. Exports would be 12.7 million bales against 7.6 million bales in the previous year. India is expected to import 1.2 million bales for the current season ending September 2012.

Based on our recent field study, we remain optimistic on the prospects for Indian yields with recent improvements in rainfall and general weather conditions.

A Slumping Market in India

For a commodity that seemed bullish following a truant monsoon, cotton has wilted due to the increasing intensity of rain in growing areas. The market has dropped by over 10% in a matter of three weeks.

Poor fundamentals in the global market are likely to put pressure on prices. Demand is lackluster despite a lower global output, a factor that may continue to impact cotton prices.

Domestic mill consumption has been reduced by power problems in South India, where the largest spinning mills are located. Lack of export demand in cotton yarn has put pressure on prices of cotton yarn. With prospects of a good cotton crop, mills are in no hurry to buy and stock cotton. Also, most of the imported cotton is yet to arrive.

Seed demand has dropped by about 10% nationally, as more and more farmers have started switching from cotton to other crops. The seed companies are pessimistic that demand will recover even after the Cabinet Committee on Economic Affairs (CCEA) revised the Minimum Support Price (MSP) for cotton on Sept. 3, 2012 by up to 28%. The hike in MSP would not make any significant impact, as market prices are ruling at par with MSP.

Cotton Quality for 2012/13

In India, there is an unwritten rule that “More the quantity, better the quality”. Whenever the crop size is more, quality of cotton is expected to be good. This rule was broken during the last cotton season. Deficiency of rains in the later part of the monsoon season resulted in lower quality of cotton especially from parts of central India. Heavy use of fertilizers and pesticides and inability to apply micronutrients resulted in lower yield and lower maturity in state of Maharashtra, the 2nd largest cotton growing state. There was a fall in the Micronaire value of cotton resulting in heavy losses to the farmers and ginning factories in the state.

The situation this year is slightly different. The rains were deficient in the early part of monsoon season (June to mid-August) but picked up later. Irrigation helped to sustain the cotton crop during the early parts of the sowing season, and the current spell of rains is now expected to help in a better yield.

As per our recent field survey, boll formation is good and there are no traces of major diseases. If the farmers are able to take preventive measures against common expected diseases like red leaf and pests like white fly, the yield and quality of Indian cotton will be good this year.

National Export/Import Policy

If events of the last two years are anything to go by, cotton is at risk of adverse policy changes, as the government will soon review its export policy for rice, wheat, sugar and cotton. Shipments abroad of these commodities might be curbed till the full harvest arrives and the festival season ends.

Their export is allowed under open general license, and there is a registration procedure for cotton. According to officials, a shortage in cotton output is expected due to erratic rain. The free export policy comes to an end in a month. The textile ministry had already recommended a ban on export until the market showed surplus availability for the domestic industry.

Stability and predictability of policy – including the export policy is critical for 2012/13, given the global demand-supply fundamentals including stocks. World cotton prices are unlikely to see a bull run despite the threat of tightening supplies. New York cotton prices are fundamentally bearish. The global impact will be felt on domestic prices.

The data for policy making needs to be as accurate as possible. Significant differences in data collection of acreage, production, consumption and stock make it difficult for the Ministry to coordinate and identify, on a real-time basis, the actual position. A cotton distribution bill with monthly collection of data in public domain, as suggested by V. Sriniwas, joint secretary of Union Textile Ministry, would be highly beneficial.

To overcome the inconsistencies in farm export-import policy, the government must allow a minimum quantity for export of select agri-commodities including cotton to help India become a stable player in the global market. Careful regulation and constant monitoring of data on monthly basis is essential for export-import policy decisions.