Shurley: Will We See Improvement in Weak Cotton Prices?

May 5, 2025

May 5, 2025 In USDA’s March 31 Prospective Plantings report, farmers said they intended to plant 9.87 million acres of cotton this year – down 12% from last year. Some industry observers expected as much as a 15% decline. I wonder now if, in fact, that’s where we’re headed. New crop prices (Dec.‘25 futures) haven’t helped.

Georgia, for example, was projected to be down only 100,000 acres, or 9% from last year. Texas is down 8%. I can’t speak with much authority about Texas, but I can tell you there sure seems to be a lot of corn and peanuts being planted here in Georgia. Which in itself seems somewhat puzzling, because even with our typically strong positive basis, is there really that much better profit potential in corn less than $5.00?

Prices (Dec.’25 futures) have crashed twice to the 65 to 66 cents area. We’ve also been teased twice with a move to around 71 cents. That led us to think that things were possibly on the mend, but prices could not hold. The key to a better outlook continues to be improved demand as evidenced by exports.

Without improved and less uncertain demand, the market, for now, is mostly (not entirely but largely) choosing to ignore U.S. acres and growing conditions. This most likely won’t last forever. The ever-changing uncertainty of current U.S. tariff policies and related concerns over economic slowdown and/or recession are also not helping.

USDA’s April supply/demand report lowered projected U.S. 2024 crop year exports by 100,000 bales – from 11.0 to 10.9 million bales. Weekly export reports show that export shipments have averaged almost 372,000 bales per week over the past five weeks.

With 14 reporting weeks remaining in the 2024 crop marketing year (ending July 31), exports need to average only approximately 186,000 bales per week to meet USDA’s latest projection of 10.9 million bales for the marketing year.

It could be supportive of eventually higher prices if shipments continue to do better than needed and USDA had to revise upward their projection. Of course, low prices might be partly the reason why export sales-to-shipments have done as well as they have. But major customers (shipment destinations) have included Vietnam, Pakistan, and Turkey. China has not been a significant buyer.

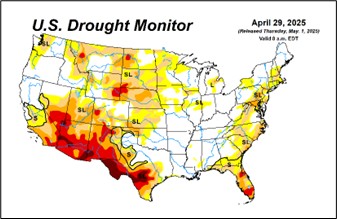

Drought conditions are present in parts of Texas, south Georgia, and the Carolinas. Dry conditions are enough to make the market somewhat sensitive to rainfall in needed areas, but it doesn’t appear yet to be enough to spike/sustain better prices.

USDA’s Acreage report on June 30 will be the first estimate of actual acres planted. Will continued disappointing prices result in acres less than the March number? Also, the crop insurance Projected Price for cotton is 69 cents. This doesn’t offer much in the way of risk management, but it is based on market price discovery. If the Harvest Price is higher (let’s hope), that will increase the coverage guarantee on a Revenue policy.

We’ve made two runs to 71 cents. We’ll have to be able to eventually clear resistance at that level before we can expect to challenge 74 cents. To do that, demand concerns must diminish, exports must continue at least on pace to meet or exceed current USDA projections, and early crop expectations must become a larger concern (less acres planted and/or worsening conditions).

Comments and opinions expressed in this article are solely those of the author.