Shurley: Cotton Continues to Need Clarity

March 17, 2019

March 17, 2019 A week or so ago, as I left early one morning for work, the fog was so bad you literally could not see how to drive. Every foot down the road at not more than 20 mph was an unknown and an accident just waiting to happen.

For 35 days, the partial U.S. government shutdown kept markets in a fog due to USDA reports and data not being available. Those reports and data are being or have been caught up now.

Now, we continue to deal with the ongoing saga and uncertainty of the US-China trade dispute and – depending on the direction talks take – the impacts on cotton and other commodities. A March 1 deadline has come and gone as trade talks have seemed to intensify and the talks extended to try and reach agreement.

Old crop futures are in the 74 to 75 cents neighborhood. After hitting lows of 71 to 73 cents in early January and again around mid-February, prices have slowly trended up. But old crop is still 8 to 10 cents below the levels of last fall, and stuck in a range of mostly 72 to 75 cents.

New crop December futures are 73 to 74 cents and have trended up since the most recent low back around mid-February. I know that the 74 cent neighborhood doesn’t sound like much of an improvement. But based on where this market could be and still might yet go, it’s an improvement. Still, right now, December seems pretty well stuck in the 72 to 75 cent range.

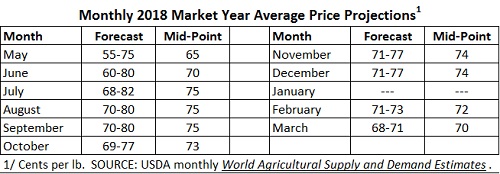

USDA announced last July that it would act to assist farmers damaged by tariffs and reduced exports. In September, the Market Facilitation Program (MFP) was initiated and the signup began. MFP payments are received on actual 2018 production.

The MPF payment rate on cotton is 6 cents per pound. The USDA projected marketing year average price for 2018 upland cotton has declined from a high of 75 cents to the most recent forecast low of 70 cents.

During this time (since the first projection back in May), the market has been impacted by the U.S. crop, a drop in projected exports, uncertainty in exports, a drop in world use/demand, and a potentially larger 2019 U.S. crop.

USDA’s March crop production and supply and demand estimates contained few changes and has pretty much been a non-factor:

- The U.S. crop was unchanged, with no change in expected exports.

- World production was raised roughly 400,000 bales, and use was lowered just slightly.

- Production was raised for Brazil and Pakistan, and lowered for Australia. The Chinese crop was unchanged.

Prices are trying to negotiate the hurdle at 75 cents. So far, the market hasn’t been able to do so. A big question will be if cotton stays in the low 70s or less, does that cause a shift in acres to be planted from cotton to another crop? USDA’s Prospective Plantings report will be out on March 29.

2018 crop year U.S. export sales to date currently stand at 13.17 million bales – 88% of the USDA projection for the marketing year. Last season we were at 94%. Actual shipments to date total 6.53 million bales – 44% of the projection, compared to 45% at this time last season.

There are uncertainties whether or not the U.S. will be able to maintain market share in exports and if the USDA 15 million bale projection can be reached. USDA has stuck with the 15 million bale number for a few months now despite these concerns.