Shurley: Acreage Report and Other Factors

July 6, 2023

July 6, 2023 Prices (new crop December futures) reached a new recent low of 77 cents – losing a little over 3 cents in three days. The new low was the lowest price since mid-December.

This move to the 77-cents area broke solid support the market had around 79 cents. As in the past, prices thankfully have since rallied (round reason to rally) back above previous support and currently stand at 79 or 80 cents after initially reaching over 81 cents.

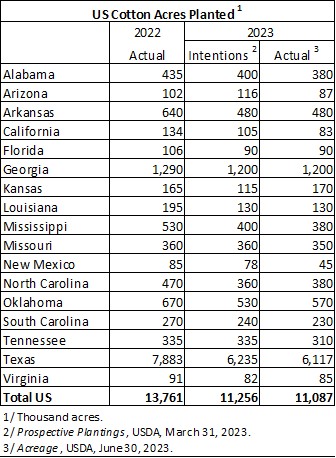

On June 30, USDA released its first official estimate of actual acres planted for 2023. As expected, actual acres planted are less than what farmers said they intended to plant back in March. However, this acreage planted (11.09 million acres – 19.4% less than last year) is still more than what some industry observers believe is out there.

Nevertheless, we all know that acres harvested and yield are more important. Reports beginning with July’s supply/demand numbers and continuing weekly and monthly thereafter will update the condition, projected harvest acres, and yield for this crop. The market will react accordingly. NOTE: the “expected” or “most likely” price range is still 79 to 86 cents. But this recent move to 77 cents now creates a little more downside and potential risk.

The crop condition index (excellent=5, good=4, 3=fair, poor=1, very poor=0) has not changed dramatically but has slipped three of the last four weeks. The index was 3.27 on July 2 versus 3.46 on June 4. The Texas crop was 32% poor-to-very poor on June 2.

Portions of West Texas and the Panhandle area have received rainfall over the past couple of weeks, but the amount is still below normal in some of those areas. In fact, precipitation has been below normal across much of the Cotton Belt. The 10-day forecast (July 6-14) is for small amounts of rain over Texas but larger amounts of rain – some heavy – over the Mid-South and Southeast.

It’s reported by some that there are new demand concerns that seem to be surfacing. Export shipments for the most previous 4-week period have averaged 271,600 bales per week. With a little over five reporting weeks left in the 2022 crop marketing year, shipments need to average roughly 355,000 bales to meet USDA’s 13 million bale projection. The export pace has slowed a bit and will need to pick up to meet the 13 million bales mark.