Shurley: Weather, Crop Reduction Give Prices Another Boost

August 19, 2023

August 19, 2023 I’ve heard one grower comment that “cotton should be $1.50.” I doubt we’ll get there, but we can always hope.

Cotton has made a good little run since the end of June, making it to the 88 cents neighborhood twice. This run took us again to the highest prices in almost a year. This level may be tested. We’ll see how much staying power it has. Any run, if it’s based on supply side factors, isn’t likely to stay unless there’s also demand (buying) at that level.

USDA’s August supply/demand numbers have attributed overall to a little more bullish tone to the market that we haven’t seen in a while.

- The upcoming 2023 U.S. crop was cut by 2½ million bales – a huge revision down in acres to be harvested and expected yield.

- But projected U.S. exports for the 2023 crop year were trimmed by 1.25 million bales, taking some of the steam out of the impacts of a smaller crop.

- Exports for the now completed 2022 crop year were cut 100,000 bales from the July estimate, attributing to an increase in carry-in stocks and, again, taking steam out of the smaller crop.

- Projected World production for 2023 was decreased, due almost entirely to the smaller U.S. crop.

- World use/demand for the 2023 crop year increased 500,000 bales. China’s use and imports were both increased from the July estimates. Use was revised up slightly for Turkey and down slightly for Indonesia.

- Exports for Brazil were increased.

This month’s USDA Crop Production report shows the Texas crop is estimated to have a 36% abandonment rate and an average yield of 518 lbs/acre, compared to 734 lbs/acre last year. Abandonment in Oklahoma is expected to be 26% with an average yield of 594 lbs/acre.

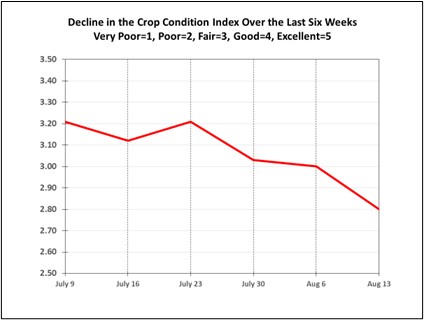

The condition of the crop dropped dramatically this past week – 2.8 compared to 3.0 the week before. Condition has been in a downtrend for weeks. As of Aug. 13, the crop was 43% poor or very poor, 21% fair, and 36% good to excellent.

Overall, the crop is on pace (only very slightly behind) in development but is behind normal in several states including California, Georgia, Louisiana, North Carolina, and South Carolina.

The export report for the week ending Aug. 3 showed a nice rebound in sales compared to the previous week but also a reduction in shipments – 34% below the previous week.

In summary, the U.S. crop looks to possibly be less than earlier estimates. While this could support a boost in price, that effect is offset somewhat by a little larger beginning stocks carried in from the ’22 crop year and reduction in projected ’23 crop year exports.

Going forward, price depends on the condition and further revision in the U.S. crop and how demand and exports are doing. China’s use and imports are both increased from prior estimates. That bodes well, but there has recently been concern about reports from China signaling economic slowdown.

December futures has come off the recent high and currently stand around 85 cents.