Shurley: Prices Refocus on Move Lower; Recovery and Upside Still Possible

April 4, 2023

April 4, 2023 In my mid-March remarks, I mentioned that prices were still in neutral and had not moved lower. As is my luck, prices then proceeded to move lower, dropping four cents over the next 10 days before making a recent recovery. We now stand in the 83 cents area for December 2023 futures – the middle range we’d previously been in for months.

USDA’s Prospective Plantings report last week came in on the high end of most pre-report expectations, yet the market seemed to shake that off with little to no impact. A good export report helped, and economic and financial fears seem to be subsiding.

So, here we are. After a scare that took us to 78 cents, the market seems to have since refocused and still has support around 81 cents, but 78 to 79 cents below that. The top appears to be 85 to 86 cents.

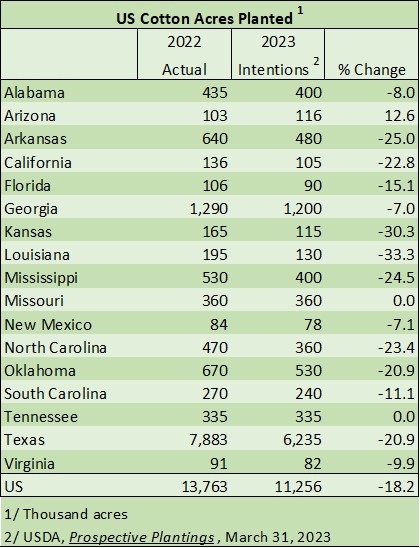

Growers say they intend to plant 11.26 million acres this year – 18% less than last year. Acreage is expected to be down in all but three states. This compares to the National Cotton Council’s survey estimate back in mid-February of 11.42 million acres and USDA’s unofficial earlier projection of 10.9 million acres during its Outlook Forum later that month.

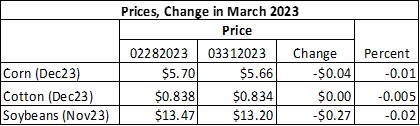

The decline in cotton acres signals cotton losing acres to competitive crops such as corn, soybeans, and in some cases, peanuts. Futures prices for cotton, corn, and soybeans were all down slightly in March. But due to last week’s recovery, cotton held its own against other crops.

We’ve now had two consecutive strong weeks of export sales and shipments. Both sales and shipments have averaged over 300,000 bales per week. This has helped overcome sometimes negative signals from other market factors. Shipments need to average roughly 279,000 bales per week to reach USDA’s current projection for the marketing year.

Prices will continue to battle to overcome demand uncertainty. Even though planted acres are expected to be down sharply, production can exceed last year depending on acres harvested and yield. Production and supply are not yet a concern.

The most recent dip in price increases downside risk. But potential on the upside is still there.