Shurley: Some Thoughts on Where We Are Now

November 23, 2020

November 23, 2020 Pricing opportunities have now moved to basis the March futures. So you may notice the futures look to be a bit higher. That’s due to the “spread” between December and March. At present, March is about 2.3 cents higher than expiring December.

Also, the basis has improved somewhat from where we were about a month ago. According to USDA-AMS, the basis quoted is currently -225 points for 31-3/34 and even the March futures for 31-3/35. This is about 50 points better than a month ago.

The market has gotten somewhat flat and is waiting on the next event. When prices are flat or sideways, it signals that neither buyers nor sellers see good reason to upset the apple cart – the market is seemingly content for the time being. Prices (March futures) are currently hovering just below 72 cents and in a channel of mostly 70 to 72 cents.

Having said that, we are at an important juncture:

- There is still uncertainty about the size of the U.S. crop

- The market is now getting antsy over what could be developing into another partial shutdown here and in other parts of the world due to increasing COVID numbers. Will the availability of vaccine ease the numbers and the uncertain outlook?

- Assuming a Biden Presidency, what would that portend for trade and for agriculture more broadly?

My point is this. If the U.S. crop does, in fact, end up in the neighborhood of 17 million bales, the last thing this market needs is concerns over world use/demand and U.S. export potential. USDA’s December numbers due in a few weeks will continue to shed light on this price discovery process.

The export numbers for the week ending November 12 were mixed and not considered strong. Net sales were only 140,100 bales – down by almost half of what they were the prior week. The largest sales were to destinations in Vietnam, Pakistan, China and Turkey. Sales were down due partly to 49,400 bales in sales cancellations – most of those in China.

Shipments for the week ending November 12 were 305,300 bales, with 138,800 bales or 45% going to China. Shipments were good, but down 6% from the prior week.

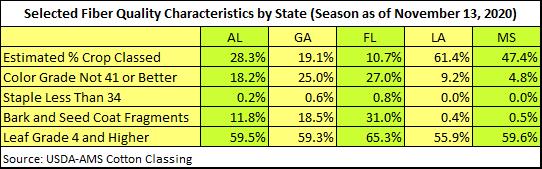

One of the concerns this year has been fiber quality in some areas, particularly the Mid-South and Southeast, due to adverse weather from hurricanes and tropical storms. Thankfully, prices have rallied from the lows of seven months ago, and the basis has improved (although only slightly). Higher prices can be eroded by discounts for fiber quality.

Below are a few summaries and comparisons tabulated from the latest available classing data.

In these five states, overall color grade appears not to be an issue. But looking more closely, the percent of the crop grading 41 in color I’m sure is higher than what growers would like to see. Staple less than 34 appears not to be an issue.

In the three Southeast states looked at, seed coat fragments are a big problem. Also, pretty much across the board, leaf grade appears to be high. In each state, over half (almost 60%) of the bales classed so far have graded a 4 Leaf or higher.

There still a ways to go with the classing of the harvest. The numbers could improve, but fiber quality typically does not improve as harvest progresses. Worth noting, based on USDA expected production for these states, bales classed to date would appear to show that the Southeast is running well behind the Mid-South. Does this reflect later harvest and thus ginning and classing…or maybe the crop in the Southeast is not as large as projected?