Shurley: Cotton Prices Remain in Neutral Despite New Information

March 17, 2023

March 17, 2023 The market has had a lot of new data and information to digest and react to in recent weeks. Some, but relatively little, seems good for prices. Nevertheless, prices show the ability to recover and remain mostly in the low to mid-80s where they’ve been for months. Prices haven’t moved lower – but also aren’t yet ready to commit to move higher.

New Crop Acreage and Production. On Feb. 12, the National Cotton Council survey estimate was 11.42 million acres planted this season. Given prices and estimated net returns comparisons with other crops, most industry observers I think expected something below 11 million. More recently on Feb. 23 at the USDA Outlook Forum, USDA economists projected 10.9 million acres planted for 2023 and a crop of 15.8 million bales based on average yield and abandonment. If realized, this would be almost 8% higher than last year.

The first official USDA “statistical” estimate of expected plantings will be USDA’s Prospective Plantings report to be released on Mar. 31. If that number is close to or less than 10.9 million acres, that should add support to the market unless overshadowed by demand concerns.

World Demand. Last week, USDA released its monthly crop production and supply/demand estimates for March. In summary:

- The U.S. crop for 2022 was unchanged from the February estimate. Projected exports for the 2022 crop year were also unchanged.

- World use (demand) was lowered 550,000 bales.

- China’s imports for the 2022 crop year were lowered 250,000 bales.

- World beginning stocks and production for 2022 were raised. So, the combined result of this and the lower demand was an increase of 2 million bales in carry-in stocks to the 2023 crop year effective Aug. 1.

Compared to other crops, cotton seems especially sensitive to economic and political factors that can be demand indicators. Most recently, U.S. economic and recession fears and political tensions with China have been destabilizing factors.

As far as price direction goes, the demand side is still the main driving force. The supply side can and likely will come into play when more is known with greater certainty, but not yet.

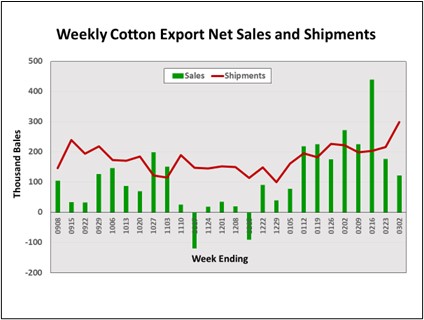

Exports. USDA projects 12 million bales in exports for the 2022 crop marketing year. Weekly export numbers are a gauge on how we’re doing toward meeting that projection. Generally, they can also be a barometer for improving or weakening World demand.

The next export report will be out on Mar. 16. The most current report, released last week, is data for the previous week ending Mar. 2.

The trend in shipments has improved over the past two months. Sales have trended down, however. But, within the past few weeks, we’ve seen marketing year highs in both weekly sales and shipments.

Lower sales are a concern, but the trend up in shipments is encouraging. In the most recent report (for the week ending Mar. 2), weekly sales to China were 17, 300 bales and shipments were 57,800 bales.

For the past four weeks, shipments averaged 229,650 bales per week – 11% higher than the previous four weeks. To meet USDA’s projection of 12 million bales export, shipments must average 284,000 bales per week. We are presently not on pace to do that, but shipments for the week ending Mar. 2 were a marketing year high of 299,100 bales.